A Day In The Life: The Investing Process

I'm sometimes asked by people who know I'm in "some sort of finance", "What do you do?" Usually the person asking wants to make what I do, since it is "some sort of finance" and most folks have an irrational aversion to numbers, seem more difficult than it really is. What I do ain't rocket science, trust me. Warren Buffett is fond of saying investing requires the math skills of a 5th grader. So I usually answer with as simple an explanation as I can muster. "I help people invest in stocks and funds," is the line I offer by rote.

Recently someone followed up with, "I mean, what do you do day to day? How do you help people invest?" Again, what I do is not that complex or exciting. My answer was, "I read." I wasn’t being flippant. It is just really the answer. I read anything I can and have time for about the companies of interest to me, philosophies on investing to philosophies about other disciplines that might help my approach to investing. Charlie Munger, the long-time partner of Buffett calls this a latticework of mental models. This is what I am trying to create with my reading.

In the past, I have talked about how my process, which is influenced by Buffett, Munger, Benjamin Graham and many less well-known investment managers, leads to superior results. That process includes:

- A commitment to a long-term investment philosophy.

- Owning a concentrated portfolio of easy to understand companies that generate high degrees cash and generate high returns on capital/equity.

- Adherence to a value-oriented approach to investing.

- Not deviating into non-profitable areas of the market or areas where competitive advantages are hard to come by (i.e. gold, shorting, or commodity trading).

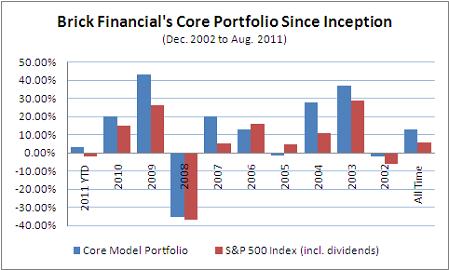

Clearly we’ve done well:

As the chart points out, our Core Portfolio has beaten the market in most calendar years and is ahead of the market so far this year. From the time of inception the portfolio’s annualized total return has been more the double that of the market’s total return (Core: 12.3% vs. S&P 500 Index: 5.1%). Over a typical working lifetime of about 40 years, 12.3% will turn a one-time $10,000 investment into $1,000,000 while a 5.1% investment will become $70,000.

A Day In The LifeThe following is an example of how my day transpires. No day is typical. It depends on the season, if school is in, if quarterly earnings are imminent. But this gives a good representation.

- 6:00am: Open emailed version of Wall Street Journal and New York Times and read articles pertinent to the positions in the portfolio. Read any other article that sparks an interest – not necessarily finance related.

- 7:00am – 8:00am: Get daughters ready for and dropped off to school.

- 8:00am: Continue reading articles and any alerts emailed to me regarding our current positions.

- 9:30am: Market opens. Check portfolio to see how our positions opened. Take any action if necessary (which rarely happens).

- 10:00am: Go to the gym.

- 11:00am (bulk of the day): Turn on the financial news, primarily for the ticker. Watch any videos on the web that pique my interest. Google/Twitter search for news relevant to our investments or investments I have my eye on. Listen to recorded quarterly conference call or read financial statements or write a blog post, etc. Hop on the train to the New York and drop in on an investment conference, especially if its free or low cost. Read or watch anything I can find by investment managers who share a value oriented approach.

- 3:00pm: Pick up girls from school.

- 4:00pm: Market closes. See how portfolio shaped up for the day. Check if any positions currently on our watchlist look like buys.

- 4:30pm – 8:30pm: Spend time with family. Help girls with homework.

- 9:00pm: Listen to recorded quarterly conference call or read financial statements or write a blog post, etc. or, Just shut it down for the day and spend that time with family or fun.

The process is not sexy and may be boring but it gets results. There is no secret formula.

Subscribe:

Email |

Reader |

RSS |

| Subscribe:

Email |

Reader |

RSS |

|

|

Digg -- submit this item to be shared and voted on by the digg community. For more about digg,

Digg -- submit this item to be shared and voted on by the digg community. For more about digg,  Del.icio.us -- mark an item as a favorite to access later or share with the del.icio.us community. For more about del.icio.us,

Del.icio.us -- mark an item as a favorite to access later or share with the del.icio.us community. For more about del.icio.us,